Dissecting all the parts of this important metric.

By

Laura Gariepy

You may have heard that having a higher credit score (or, technically, SCORES, as we all have multiple) increases your chances of getting approved for a loan and receiving better credit terms - think lower annual percentage rates (APRs), better rewards, etc. So, what factors make up your credit scores anyway?

Since there are so many moving parts involved, we thought we’d break it down for you. While we can’t tell you exactly what contributes to your specific scores, we can outline some of the main factors that commonly impact a credit score. That way, you’ll have a better idea of what financial behaviors can help you, or hurt you, as you consider your own credit.

First, let’s zoom out to take a look at the larger credit ecosystem. There are three major consumer credit reporting agencies (CRAs), or credit bureaus, in the United States: Equifax, TransUnion, and Experian. There are also other smaller and specialty credit bureaus. Each credit bureau uses different models, or score cards, to determine someone’s credit score, which means one person could have many different credit scores.

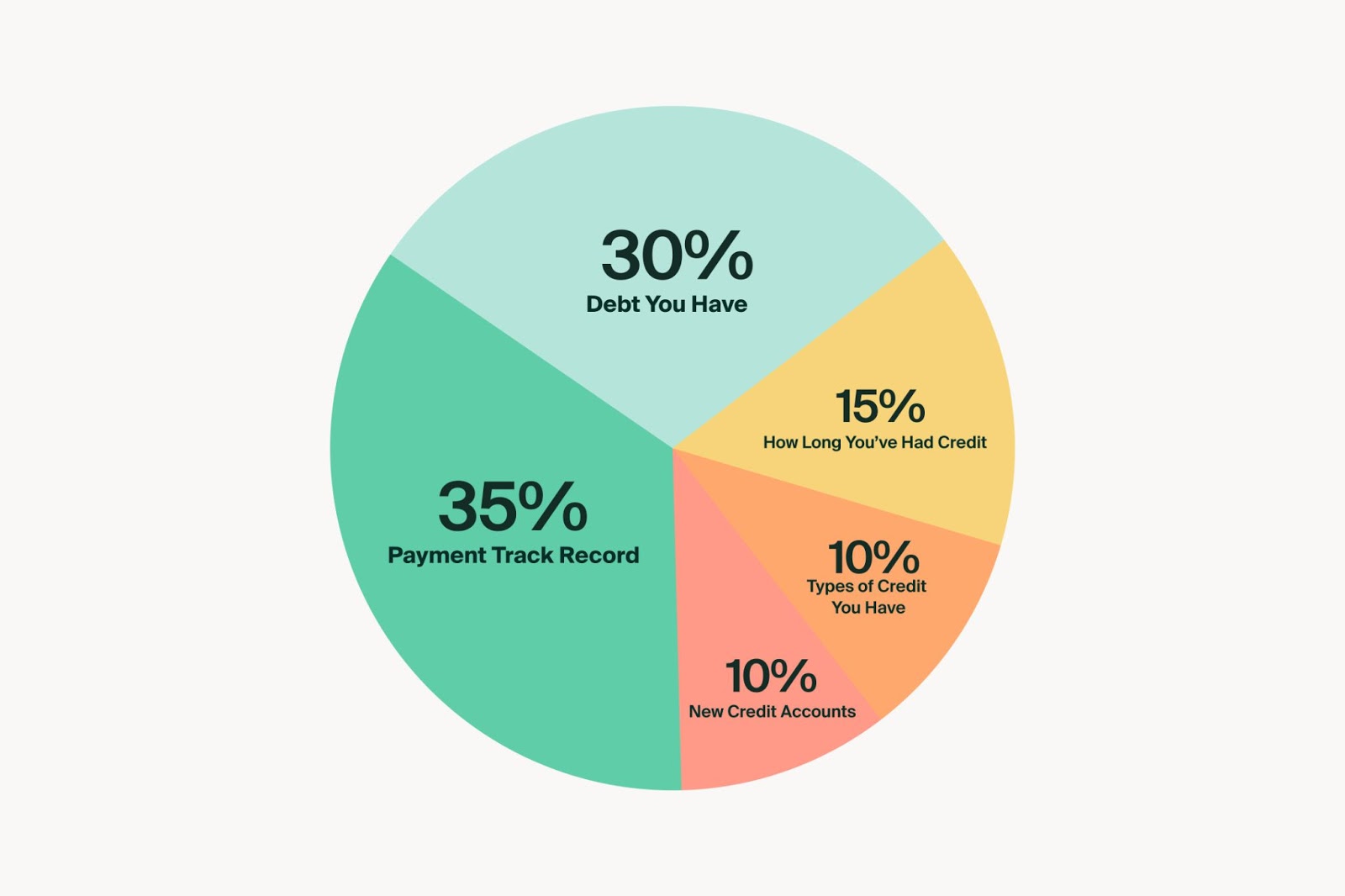

Even with these differences in models, though, there are five main factors that are commonly considered in deciding a credit score.

Please remember: The following percentages give you a rough idea of how much weight each element carries.

Your payment track record, or payment history, commonly has the biggest impact on a credit score. In fact, while the exact effect on a score depends on the credit bureau's model, payment history can account for up to 35% of your total rating. Accounts factored into your payment history can include credit card, installment loan (car loan), mortgage payment, and finance company accounts. Your creditors track and report each payment you make to the credit bureaus. While late or missed payments could cause your score to drop, timely payments month after month demonstrate financial responsibility and can translate into a higher score.

How much credit you use in relation to your total available credit across accounts (aka your credit utilization) can have a major impact on a credit score, too, and may account for up to 30% of your total rating. Lenders want to see that your level of debt doesn’t indicate you might have trouble making your monthly payments on time and that you’re not maxing out your accounts. Why? Higher levels of debt, or using significant amounts of your available credit, could indicate that you’re strapped for cash, which could make it difficult for you to repay a new loan. As a general rule, many credit experts recommend keeping your utilization under 30%. That means, if you have a combined $1,000 credit limit across two credit cards, keeping your total amount owed at $300 or less may reflect positively in your credit score.

Note: If you have multiple credit cards, keeping low to zero balances on one or two may help lower your overall utilization. However, not using your account and keeping your credit balance at $0.00 for too long may result in an inactive account closure, which could negatively affect your credit score.

Remember, while paying down (and eventually off) your mortgage or car loan is a good goal, how much you owe doesn’t typically impact your credit score.

How long you’ve had credit, or the length of your credit history, takes a backseat to your payment history and credit utilization. But, coming in at roughly 15% of a credit score, it’s still a significant factor. This component considers the length of your credit history, including the age of your oldest credit account, the age of your newest credit account, and the average age of all of your credit accounts; and account usage. In general, the longer your credit history, the better it is for your score because you’ve had ample opportunity to demonstrate responsible credit behaviors and indicate you’re a low-risk borrower. As long as you manage your credit accounts responsibly, time is your friend.

Believe it or not, the types of credit accounts you have matter. This is commonly called your credit mix. This component can make up approximately 10% of a credit score. Lenders like to see that you can dependably handle a variety of financial obligations that include both revolving lines of credit (think credit cards) and installment loans (think mortgages, car loans, or student loans). If you maintain a healthy mix of credit accounts and manage them responsibly, you could see your credit score grow.

In short: Over time, try to build a credit history that features a variety of accounts while only applying for the credit you truly need (not simply for the sake of credit mix).

Also coming in at around 10%, the number of new credit accounts you open can also have an impact on your score. When you apply for a new credit card or loan, a lender usually pulls your credit, which can cause a small dip in your credit score. If your application is approved, and you decide to accept the loan, your credit score may take another dip.

Why? Multiple new applications or loans might indicate you’ve taken on too many financial obligations. Translation: If a lender sees a lot of credit pulls or new accounts, they may think it’s too risky to lend you money because you could be spreading yourself too thin financially. Fortunately, inquiries for mortgages or car loans are often lumped together, so they generally have less of an impact on your credit.

Together, new applications and loans can appear on your credit reports for up to two years, and could negatively impact your credit for up to one year. Sometimes the type of credit you’re applying for impacts the weight of this factor.

The bottom line: Be thoughtful about applying for new credit accounts and only apply for the credit you need.

As you can see, the credit score is multifaceted. Now that you know about each of the five components that commonly make up credit scores, you’re better equipped to work towards the scores you want or need.

Remember: while your Mission Lane credit card is just one element that impacts your scores, using it responsibly over time can help you build your credit.

Related Reading: Want to dive deeper into these five components? Check out this myFICO article for more information.

©2023 Mission Lane LLC. All rights reserved. NMLS #1857501.

The Mission Lane Visa™ Credit Card is issued by Transportation Alliance Bank, Inc. dba TAB Bank, Member FDIC, or WebBank, pursuant to a license from Visa U.S.A. Inc.

Visa is a registered trademark of Visa U.S.A. Inc. All other trademarks and service marks belong to their respective owners.

Mission Lane LLC provides services for your Account, but is not a bank. The bank issuing your card will be identified on the back of your Visa Card and in your Cardholder Agreement, which governs your use of the Account.

Mission Lane LLC does business in Arizona under the trade name Mission Lane Card Services LLC. All trademarks not belonging to Mission Lane are the property of their respective owners.

THIS IS A LOAN SOLICITATION ONLY. MISSION LANE LLC IS NOT THE LENDER. INFORMATION RECEIVED WILL BE SHARED WITH ONE OR MORE THIRD PARTIES IN CONNECTION WITH YOUR LOAN INQUIRY. THE LENDER MAY NOT BE SUBJECT TO ALL VERMONT LENDING LAWS. THE LENDER MAY BE SUBJECT TO FEDERAL LENDING LAWS.